Federal Reserve Rate Impact: 2026 Mortgage Market Forecast

The housing market is a dynamic and complex ecosystem, heavily influenced by a myriad of economic factors. Among these, the decisions made by the Federal Reserve stand as a colossal determinant, particularly when it comes to the trajectory of mortgage rates 2026. As we inch closer to 2026, prospective homebuyers, current homeowners, and investors alike are keenly watching the horizon, attempting to decipher how the Fed’s monetary policy will shape the affordability and accessibility of homeownership. This comprehensive guide aims to peel back the layers of this intricate relationship, providing a detailed forecast and actionable insights into what the future holds for the mortgage market.

Understanding the Federal Reserve’s role is paramount. The Fed, as the central banking system of the United States, wields significant power over the nation’s economy through its monetary policy. Its primary tools include adjusting the federal funds rate, engaging in open market operations, and setting reserve requirements for banks. While the Fed does not directly set mortgage rates, its decisions on the federal funds rate have a profound, albeit indirect, impact on the interest rates offered by lenders for home loans. This ripple effect is what makes the Fed’s stance so crucial for anyone navigating the housing market.

The year 2026 is still a little way off, but economic forecasting requires looking ahead, anticipating trends, and understanding the underlying mechanisms that drive market movements. The current economic climate, characterized by ongoing inflation concerns, labor market dynamics, and global geopolitical events, provides the backdrop against which the Fed will make its decisions. These decisions, in turn, will be the primary drivers behind the direction of mortgage rates 2026. This article will delve into the historical context of Fed actions, analyze current economic indicators, and project potential scenarios for mortgage rates in the coming years, offering a clearer picture of what to expect.

The Federal Reserve’s Mandate and Its Influence on Interest Rates

The Federal Reserve operates under a dual mandate: to achieve maximum employment and maintain stable prices (i.e., control inflation). To accomplish these goals, the Fed utilizes various tools, with the federal funds rate being the most prominent. The federal funds rate is the target rate for overnight lending between banks. While it’s an overnight rate, changes to it have a cascading effect throughout the financial system.

How the Federal Funds Rate Affects Mortgage Rates

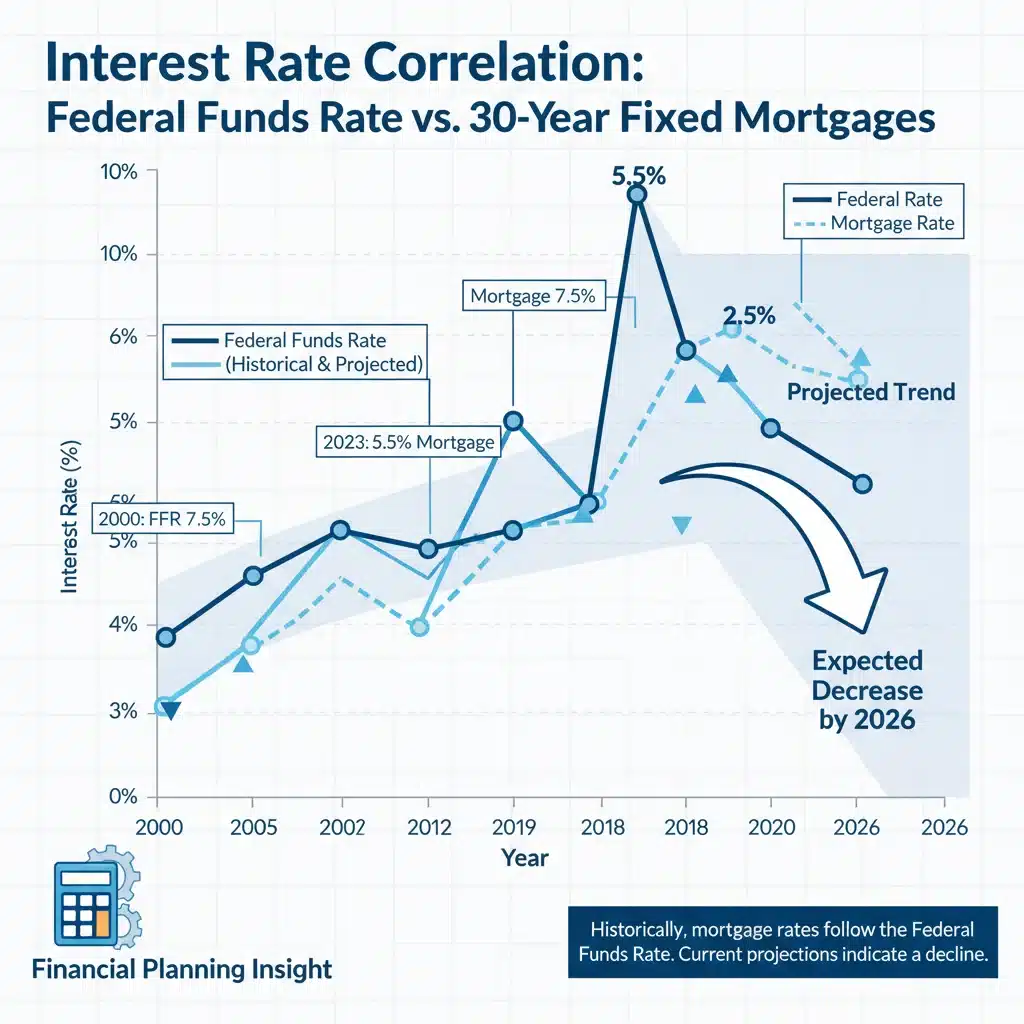

When the Federal Reserve raises the federal funds rate, it generally makes borrowing more expensive for banks. This increased cost is then passed on to consumers and businesses in the form of higher interest rates on various loans, including credit cards, auto loans, and crucially, mortgages. Conversely, when the Fed lowers the federal funds rate, borrowing becomes cheaper, leading to lower interest rates across the board.

It’s important to note that mortgage rates, particularly for long-term fixed-rate mortgages, are not directly tied to the federal funds rate. Instead, they tend to track the yield on the 10-year Treasury bond. However, the federal funds rate still plays a significant indirect role. Market participants, including those who trade in Treasury bonds, anticipate future Fed actions. If the Fed signals a hawkish stance (i.e., a propensity to raise rates), bond yields tend to rise in anticipation of higher future short-term rates, which then pushes up mortgage rates. Conversely, a dovish stance (a propensity to lower rates) can lead to lower bond yields and, consequently, lower mortgage rates.

The relationship is complex and influenced by market sentiment, inflation expectations, and global economic conditions. However, the underlying principle remains: the Federal Reserve’s overarching monetary policy direction is a primary driver of the general level of interest rates in the economy, including those for mortgages. Therefore, any discussion about mortgage rates 2026 must begin with an analysis of the Fed’s likely path.

Current Economic Landscape and Fed’s Recent Actions

To project mortgage rates 2026, we must first understand the current economic environment and the Federal Reserve’s recent responses. The past few years have been marked by unprecedented economic volatility, largely stemming from the COVID-19 pandemic and its aftermath. We witnessed a period of extremely low interest rates, designed to stimulate economic activity during the pandemic-induced downturn. This led to a boom in the housing market, with historically low mortgage rates fueling demand and driving up home prices.

Inflationary Pressures and Rate Hikes

However, the rapid economic recovery, coupled with supply chain disruptions and robust consumer demand, ignited significant inflationary pressures. Inflation soared to multi-decade highs, prompting the Federal Reserve to embark on an aggressive campaign of interest rate hikes. These hikes were aimed at cooling down the economy, bringing inflation back down to the Fed’s target of 2%. Each increase in the federal funds rate sent ripples through the financial markets, contributing to a significant rise in mortgage rates from their pandemic-era lows.

As of late, the Fed has shown signs of potentially slowing or pausing its rate hike cycle, as inflation has begun to show signs of moderating. However, the battle against inflation is far from over, and the Fed remains vigilant. Future decisions will hinge on incoming economic data, particularly inflation reports, employment figures, and consumer spending trends. The Fed’s commitment to its dual mandate means it will continue to adjust its policies as necessary to achieve its objectives.

The current landscape is one of careful observation and data dependency. The Fed’s forward guidance, statements from its officials, and the minutes of its meetings are all scrutinized by market participants for clues about future policy moves. These clues are essential for forecasting where mortgage rates 2026 might land.

Forecasting Mortgage Rates 2026: Key Factors to Consider

Predicting mortgage rates more than a year out is inherently challenging due to the multitude of unpredictable variables. However, by analyzing key economic indicators and understanding the Fed’s likely responses, we can develop informed projections for mortgage rates 2026. Here are the primary factors that will shape the Fed’s decisions and, consequently, mortgage rates:

1. Inflation Trajectory

This is arguably the most critical factor. If inflation continues its downward trend and approaches the Fed’s 2% target, it could provide the central bank with the flexibility to pause or even begin to cut interest rates. Conversely, if inflation proves to be stickier than anticipated, or if there’s a resurgence, the Fed might be compelled to maintain higher rates for longer, or even implement further hikes. The path of inflation will be the guiding star for the Fed’s policy in the lead-up to 2026.

2. Labor Market Conditions

A strong labor market, characterized by low unemployment and robust wage growth, can contribute to inflationary pressures as consumers have more disposable income. If the labor market remains exceptionally tight, the Fed might feel less urgency to cut rates, even if inflation moderates. Conversely, a significant weakening of the labor market could prompt the Fed to consider rate cuts to support economic growth, which would likely push mortgage rates 2026 lower.

3. Economic Growth and Recession Risks

The overall health of the economy is another vital consideration. If economic growth slows significantly or if there’s a risk of recession, the Fed might opt for a more accommodative monetary policy (i.e., lower rates) to stimulate activity. A robust economy, on the other hand, might allow the Fed to maintain a tighter stance without fear of stifling growth too much.

4. Global Economic Factors

The U.S. economy does not operate in isolation. Global economic developments, such as geopolitical tensions, commodity price fluctuations, and the economic performance of major trading partners, can all influence the Fed’s decisions. For example, a global economic slowdown could dampen demand and ease inflationary pressures, potentially leading to lower mortgage rates 2026.

5. Fiscal Policy

Government spending and taxation policies (fiscal policy) can also impact the Fed’s monetary policy. Large government deficits and increased spending can be inflationary, potentially requiring the Fed to maintain a tighter monetary stance. Conversely, fiscal austerity could help to curb inflation, giving the Fed more room to ease policy.

Potential Scenarios for Mortgage Rates 2026

Given the interplay of these factors, we can outline a few plausible scenarios for mortgage rates 2026:

Scenario 1: Soft Landing and Moderate Rate Cuts

In this optimistic scenario, inflation continues to cool gradually, and the economy avoids a severe recession. The Fed, seeing its inflation targets within reach, begins to implement moderate rate cuts in late 2024 or early 2025. This would lead to a gradual decline in mortgage rates throughout 2025 and into 2026, making homeownership more affordable. Mortgage rates might settle in a range slightly above the pre-pandemic lows but significantly below the peaks seen during the aggressive rate hike cycle.

Scenario 2: Persistent Inflation and Higher for Longer Rates

This scenario assumes that inflation proves more stubborn than anticipated, perhaps due to renewed supply chain issues, geopolitical events, or continued strong demand. In this case, the Fed would be compelled to maintain its restrictive monetary policy for longer, potentially even implementing further modest rate hikes if inflation reaccelerates. This would mean mortgage rates 2026 remain elevated, potentially hovering around current levels or even ticking higher, posing challenges for housing affordability.

Scenario 3: Economic Downturn and Aggressive Rate Cuts

In a less favorable scenario, the economy experiences a significant downturn or a deeper recession. This could be triggered by various factors, such as a credit crunch, a sharp decline in consumer spending, or a global economic shock. In response, the Federal Reserve would likely implement aggressive rate cuts to stimulate the economy, bringing mortgage rates 2026 down considerably. While lower rates would be a silver lining for homebuyers, they would come at the cost of a weaker overall economy and potential job losses.

It’s crucial to remember that these are scenarios, not definitive predictions. The actual path of mortgage rates 2026 will depend on how the economic data unfolds and how the Federal Reserve reacts to it. Staying informed about economic reports and Fed communications will be key to understanding which scenario is most likely to materialize.

Impact on Homebuyers and Homeowners

The trajectory of mortgage rates 2026 will have significant implications for various participants in the housing market:

For Prospective Homebuyers

- Affordability: Lower mortgage rates directly translate to lower monthly mortgage payments, making homeownership more affordable. This could bring more buyers into the market, especially first-time homebuyers who are highly sensitive to interest rate fluctuations.

- Buying Power: With lower rates, buyers can qualify for larger loan amounts for the same monthly payment, effectively increasing their buying power.

- Market Competition: A significant drop in rates could reignite competition in the housing market, potentially leading to bidding wars and faster home price appreciation, especially in desirable areas.

For Current Homeowners

- Refinancing Opportunities: If mortgage rates 2026 decline significantly, many homeowners could find opportunities to refinance their existing mortgages at lower rates, reducing their monthly payments and saving money over the life of the loan.

- Home Equity: Stable or appreciating home prices, often supported by lower rates, can increase homeowners’ equity, providing opportunities for cash-out refinances or home equity loans.

- Selling Decisions: Homeowners looking to sell might find a more robust buyer pool if rates are lower, potentially leading to quicker sales and better offers. However, if they are also buying a new home, they will face the same market conditions as other buyers.

For Real Estate Investors

- Rental Market: Lower mortgage rates can make it more attractive to purchase investment properties, potentially increasing the supply of rental units. However, if homeownership becomes more accessible, it could reduce demand for rentals.

- Property Values: A favorable interest rate environment generally supports higher property values, which can be beneficial for investors holding real estate assets.

- Financing Costs: Investors often rely on financing for their acquisitions. Lower rates reduce their cost of capital, making investments more profitable.

Strategies for Navigating the 2026 Mortgage Market

Regardless of which scenario for mortgage rates 2026 ultimately unfolds, there are proactive steps individuals can take to position themselves advantageously:

For Prospective Buyers:

- Improve Your Credit Score: A strong credit score is always beneficial, as it can qualify you for the best available interest rates. Start working on this well in advance.

- Save for a Down Payment: A larger down payment reduces the amount you need to borrow, which can mitigate the impact of higher interest rates.

- Get Pre-Approved: Understanding how much you can afford and getting a pre-approval will put you in a stronger negotiating position when you find a home.

- Consider Adjustable-Rate Mortgages (ARMs) Carefully: While fixed-rate mortgages offer stability, ARMs might offer lower initial rates. However, be aware of the risks associated with rate adjustments in the future.

- Work with a Knowledgeable Lender: A good mortgage professional can help you navigate different loan products and advise you on the best options for your financial situation.

For Current Homeowners:

- Monitor Rates: Keep an eye on mortgage rates 2026. If they drop significantly, evaluate whether refinancing makes sense for your situation.

- Assess Your Equity: Understand how much equity you have in your home. This can be a valuable asset for various financial goals.

- Pay Down Principal: Even small extra payments towards your principal can save you a significant amount in interest over the life of the loan.

The Role of Economic Data and Expert Analysis

Given the data-dependent nature of the Federal Reserve’s policy, staying informed about economic releases is crucial. Key reports to watch include:

- Consumer Price Index (CPI): The primary measure of inflation.

- Producer Price Index (PPI): Measures inflation at the wholesale level.

- Jobs Report (Non-Farm Payrolls, Unemployment Rate): Provides insights into the health of the labor market.

- GDP (Gross Domestic Product) Reports: Indicates the overall economic growth rate.

- Retail Sales: Reflects consumer spending patterns.

In addition to economic data, paying attention to statements and speeches from Federal Reserve officials can provide valuable clues about their thinking and future policy direction. Economic analysts and financial institutions also regularly publish forecasts for mortgage rates 2026, which can offer a range of perspectives to consider.

Conclusion: Preparing for the Future of Mortgage Rates

The future of mortgage rates 2026 is inextricably linked to the Federal Reserve’s ongoing battle against inflation and its commitment to fostering a stable and strong economy. While precise predictions are impossible, understanding the key drivers and potential scenarios empowers individuals to make more informed decisions.

Whether you are planning to buy a home, considering refinancing, or investing in real estate, keeping a close watch on economic indicators, Fed communications, and expert analyses will be paramount. The housing market is always in flux, but with diligent preparation and a clear understanding of the forces at play, you can navigate the landscape of mortgage rates 2026 with greater confidence and strategic foresight. The half-percentage point impact mentioned in the initial prompt serves as a reminder of how even seemingly small adjustments by the Fed can have tangible effects on the financial commitments of millions. Proactive planning is not just advisable; it’s essential.