Federal Student Loan Forgiveness 2026: Expanded Eligibility & New Opportunities

Federal Student Loan Forgiveness 2026: Expanded Eligibility and New Opportunities on the Horizon

The landscape of higher education finance is constantly evolving, and for millions of Americans burdened by student loan debt, every change brings a mix of hope and apprehension. As we look ahead to 2026, significant new legislation is poised to reshape the future of federal student loan forgiveness. This landmark bill is designed to expand eligibility for existing programs by a remarkable 15%, offering a lifeline to a broader segment of the population struggling with educational debt. This comprehensive guide will delve into the intricacies of these changes, helping you understand what the expanded student loan forgiveness 2026 means for you, how to navigate the new requirements, and what steps you can take to prepare.

For years, the promise of student loan forgiveness has been a complex and often frustrating journey for many. While various programs exist, strict eligibility criteria and bureaucratic hurdles have limited their reach. The new legislation aims to address these shortcomings, making debt relief more accessible and equitable. This isn’t just about minor tweaks; it’s a fundamental shift that could impact the financial well-being of millions, potentially freeing up significant disposable income and stimulating economic growth. Understanding the nuances of this expanded eligibility is crucial for anyone currently holding federal student loans or considering higher education in the coming years.

This article will serve as your ultimate resource for everything you need to know about the upcoming changes to student loan forgiveness 2026. We’ll explore the specific provisions of the new legislation, break down who qualifies, and discuss the potential long-term implications for borrowers and the economy. Our goal is to provide clear, actionable information, empowering you to make informed decisions about your financial future.

Understanding the New Legislation: A Paradigm Shift in Federal Student Loan Forgiveness

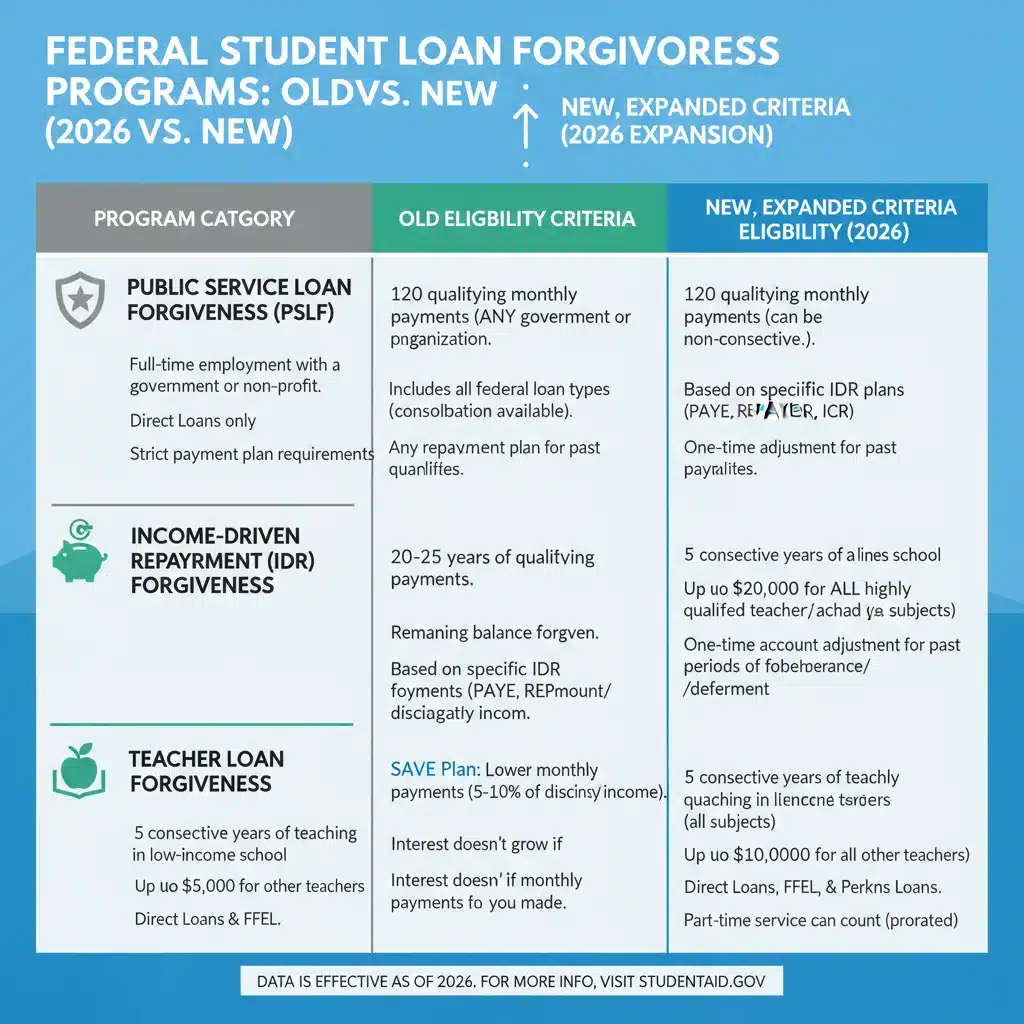

The new legislation, officially titled the "Access and Opportunity in Education Act of 2025," is a comprehensive package designed to enhance and streamline federal student loan forgiveness programs. Its primary objective is to broaden the scope of existing initiatives, particularly those related to public service, income-driven repayment (IDR) plans, and specific hardship cases. The headline figure – a 15% expansion in eligibility – represents a significant increase in the number of borrowers who could potentially qualify for relief. This expansion is not uniform across all programs but rather targets areas where the previous criteria were deemed too restrictive or failed to adequately address the needs of certain borrower groups.

Key Provisions of the "Access and Opportunity in Education Act of 2025"

- Expanded Public Service Loan Forgiveness (PSLF) Eligibility: One of the most impactful changes targets the Public Service Loan Forgiveness program. Historically, PSLF has been notoriously difficult to navigate, with many eligible borrowers being denied due to technicalities. The new legislation simplifies employer certification, broadens the definition of "qualifying employment" to include more non-profit and government roles, and introduces a more flexible payment tracking system. This means that more individuals working in vital public service sectors – from teachers and nurses to social workers and first responders – will find it easier to meet the requirements for student loan forgiveness 2026.

- Reformed Income-Driven Repayment (IDR) Plans: IDR plans are designed to make monthly payments affordable based on a borrower’s income and family size, with any remaining balance forgiven after 20 or 25 years of payments. The new legislation introduces a revised IDR plan that significantly reduces discretionary income calculations for lower-income borrowers, making monthly payments even more manageable. Furthermore, it accelerates the timeline for forgiveness for certain low-balance borrowers and addresses the issue of interest capitalization, which often caused loan balances to grow even while borrowers were making payments.

- Targeted Forgiveness for Specific Hardship Cases: The bill also carves out new pathways for forgiveness for borrowers facing severe financial hardship, including those with disabilities that prevent gainful employment, victims of institutional fraud, and individuals who have defaulted on their loans due to unforeseen circumstances. These targeted provisions aim to provide a safety net for the most vulnerable borrowers, ensuring that a path to relief exists even in dire situations.

- Streamlined Application Process: A common complaint among borrowers has been the complexity and opaqueness of the application process for forgiveness programs. The new legislation mandates the creation of a centralized, user-friendly online portal for all federal student loan forgiveness applications, coupled with clearer guidelines and improved customer support. This streamlining is expected to reduce the administrative burden on borrowers and increase the overall success rate of applications for student loan forgiveness 2026.

These provisions represent a concerted effort to make federal student loan forgiveness more effective, accessible, and fair. The goal is to ensure that educational debt does not become an insurmountable barrier to economic mobility and personal well-being. By expanding eligibility and simplifying processes, the government aims to alleviate some of the financial pressure on millions of Americans, allowing them to invest in their futures, contribute to the economy, and pursue their career aspirations without the constant shadow of overwhelming debt.

Who Benefits from the Expanded Student Loan Forgiveness 2026?

The 15% increase in eligibility is not just a statistic; it translates into real relief for a diverse group of borrowers. While the exact numbers will become clearer as the legislation is fully implemented, several key demographics are expected to benefit significantly from the expanded student loan forgiveness 2026.

Public Service Professionals

As mentioned, those in public service roles will see the most immediate and substantial impact. The revised PSLF criteria will likely bring a wave of new applicants into the program. This includes:

- Educators: Teachers, school administrators, and support staff in public and non-profit schools.

- Healthcare Workers: Nurses, doctors, therapists, and administrative staff at non-profit hospitals and clinics.

- Government Employees: Federal, state, local, and tribal government workers in various capacities.

- Non-Profit Sector Workers: Employees of 501(c)(3) organizations and other non-profits previously excluded due to narrow definitions.

- First Responders: Police officers, firefighters, and paramedics in public service.

The simplification of employment certification is particularly critical here. Many public service workers previously missed out on PSLF due to errors in paperwork or misunderstandings about "qualifying payments." The new system aims to rectify these past issues and provide a clearer path to forgiveness.

Low- to Middle-Income Borrowers

The reforms to Income-Driven Repayment plans will offer substantial relief to borrowers struggling to make ends meet. By adjusting the discretionary income calculation, a larger portion of their income will be protected, leading to lower monthly payments and a quicker path to forgiveness. This is especially beneficial for:

- Recent Graduates: Those beginning their careers with modest salaries.

- Borrowers in Underpaid Professions: Individuals working in fields that require higher education but do not offer commensurate salaries.

- Single Parents and Families: Households with higher expenses and limited income.

- Individuals with High Debt-to-Income Ratios: Those whose student loan payments consume a significant portion of their monthly budget.

The new IDR framework is designed to prevent loan balances from ballooning due to accruing interest, a common frustration for borrowers on existing IDR plans. This change alone could save borrowers thousands of dollars over the life of their loans.

Borrowers Facing Unique Hardships

The targeted forgiveness provisions will provide a much-needed safety net for those in dire circumstances. This includes:

- Borrowers with Disabilities: Individuals whose physical or mental disabilities prevent them from engaging in substantial gainful activity. The process for Total and Permanent Disability (TPD) discharge is expected to become more accessible.

- Victims of Fraudulent Institutions: Students who attended schools that engaged in deceptive practices or closed abruptly, leaving them with worthless degrees and significant debt.

- Defaulted Borrowers: The legislation includes pathways for certain defaulted borrowers to rehabilitate their loans and qualify for forgiveness, offering a fresh start.

By addressing these specific hardship cases, the government acknowledges that not all debt is created equal and that certain situations warrant direct intervention and relief. This holistic approach ensures that the expanded student loan forgiveness 2026 reaches those who need it most.

Preparing for Student Loan Forgiveness 2026: Your Action Plan

While 2026 might seem a ways off, proactive preparation is key to maximizing your chances of benefiting from the expanded student loan forgiveness 2026 programs. Waiting until the last minute could lead to missed opportunities or delays. Here’s a step-by-step action plan to help you get ready:

1. Understand Your Loan Types and Servicer

Not all student loans are federal, and only federal loans are eligible for these forgiveness programs. First, identify if your loans are federal (Direct Loans, FFEL Program loans held by the Department of Education, Perkins Loans held by the Department of Education) or private. You can check your federal loan status on the National Student Loan Data System (NSLDS) at StudentAid.gov. Also, know who your loan servicer is, as they will be your primary point of contact for application processes and information.

2. Consolidate Your Loans if Necessary

Some older federal loans (like certain FFEL or Perkins loans) might not directly qualify for all forgiveness programs, especially PSLF. Consolidating these into a Direct Consolidation Loan can make them eligible. This process can take time, so it’s wise to consider it sooner rather than later. Be aware that consolidation resets your payment count for IDR and PSLF, but with the new legislation, there might be provisions to count past payments. Always consult with your loan servicer or a trusted financial advisor before consolidating.

3. Review Your Employment History (Especially for PSLF)

If you believe you might qualify for PSLF under the expanded criteria, start gathering documentation of your past and current employment. This includes W-2s, pay stubs, and any official employment verification letters. The new legislation aims to simplify this, but having your records in order will expedite the process. Pay close attention to the updated definition of "qualifying employment" to see if your past roles now fit the bill.

4. Re-evaluate Your Income-Driven Repayment (IDR) Plan

If you’re currently on an IDR plan, or if you believe you would benefit from one, review your current plan and compare it with the proposed changes for 2026. The new IDR framework could offer lower monthly payments and a quicker path to forgiveness. Ensure your income and family size information is up-to-date with your loan servicer. Familiarize yourself with the new discretionary income calculation methods.

5. Stay Informed and Monitor Official Announcements

The implementation of such large-scale legislation takes time, and specific details may be refined closer to 2026. Regularly check official government websites like StudentAid.gov and reliable financial news sources for updates. Sign up for email alerts from the Department of Education. Be wary of scams that promise immediate or guaranteed forgiveness for a fee; legitimate forgiveness programs do not require payment to apply.

6. Consult with a Financial Advisor or Student Loan Expert

Given the complexity of student loan programs, seeking personalized advice can be invaluable. A qualified financial advisor or student loan expert can help you assess your specific situation, understand which programs you qualify for, and guide you through the application process. They can also help you develop a comprehensive financial plan that incorporates these new forgiveness opportunities.

7. Update Your Contact Information

Ensure your loan servicer has your most current mailing address, email address, and phone number. This is crucial for receiving important updates, application forms, and any correspondence related to your eligibility for student loan forgiveness 2026.

The Economic and Social Impact of Expanded Forgiveness

The implications of the expanded student loan forgiveness 2026 extend far beyond individual borrowers. This legislation is expected to have a significant ripple effect on the broader economy and society as a whole.

Economic Stimulus

When borrowers are relieved of their student loan burden, they often have more disposable income. This can lead to increased spending on goods and services, investments in homes and businesses, and greater participation in the economy. The influx of freed-up capital could provide a much-needed stimulus, particularly in sectors that have been slow to recover. It could also alleviate pressure on the housing market, as more young professionals are able to save for down payments.

Reduced Financial Stress and Improved Well-being

Student loan debt has been linked to significant psychological stress, impacting mental health, career choices, and family planning. By offering a clearer path to forgiveness, the new legislation aims to reduce this burden, allowing individuals to pursue careers they are passionate about, start families, and generally improve their quality of life. This reduction in stress can lead to a more productive workforce and a healthier society.

Enhanced Public Service Recruitment

The improvements to PSLF are particularly important for recruiting and retaining talent in critical public service sectors. When individuals know that their dedication to public service will be recognized with debt relief, it makes these often underpaid but vital professions more attractive. This could lead to a stronger public education system, better healthcare, and more robust community services.

Equity and Access to Education

The expanded eligibility also addresses issues of equity in education. Historically, borrowers from disadvantaged backgrounds or those who attended for-profit institutions have often struggled the most with student loan debt. By providing more accessible forgiveness options, the legislation aims to level the playing field, ensuring that higher education remains a pathway to opportunity rather than a source of perpetual debt for all, regardless of their socioeconomic background.

Challenges and Criticisms

While the expanded student loan forgiveness 2026 is largely welcomed, it is not without its challenges and criticisms. Concerns have been raised about the potential cost to taxpayers, the fairness to those who have already paid off their loans, and the possibility that it might encourage future borrowing without addressing the root causes of rising tuition costs. Policymakers will need to carefully monitor the implementation and long-term effects to ensure the program achieves its intended goals without creating unintended negative consequences. It will be crucial to balance the immediate relief with sustainable long-term solutions for higher education funding.

Long-Term Outlook for Student Loan Debt and Forgiveness

The "Access and Opportunity in Education Act of 2025" is a significant step, but it’s important to view it within the broader context of the ongoing debate about higher education costs and student debt. While the expanded student loan forgiveness 2026 offers substantial relief, it doesn’t fully resolve the underlying issues that contribute to the student debt crisis.

Addressing the Root Causes

For sustainable change, future efforts will likely need to focus on controlling tuition costs, increasing state funding for public universities, and reforming the financial aid system to emphasize grants over loans. Without addressing these fundamental issues, new generations of students may continue to face similar debt burdens, even with enhanced forgiveness programs. The current legislation provides a crucial bandage, but a more holistic approach is needed for a permanent cure.

Continuous Program Evaluation

It’s reasonable to expect that the effectiveness and efficiency of these expanded programs will be continuously evaluated. Data on borrower outcomes, economic impacts, and administrative costs will inform future policy adjustments. This iterative process is essential to ensure that federal student loan programs remain responsive to the needs of borrowers and the evolving economic landscape. The 2026 changes are a major step, but likely not the final word on student loan reform.

Borrower Responsibility and Financial Literacy

Even with expanded forgiveness, borrowers still have a crucial role to play in managing their educational debt. Financial literacy – understanding loan terms, repayment options, and the implications of borrowing – remains paramount. The government and educational institutions also have a responsibility to provide clearer, more accessible information to prospective and current students, empowering them to make informed decisions about their education and finances. The goal is to create a system where students can pursue their educational dreams without fear of being crushed by insurmountable debt, and expanded student loan forgiveness 2026 is a key component of that vision.

Conclusion: A New Era for Student Loan Forgiveness

The impending changes to federal student loan forgiveness in 2026 mark a pivotal moment for millions of Americans. The "Access and Opportunity in Education Act of 2025" is set to expand eligibility by 15%, offering unprecedented relief through reformed Public Service Loan Forgiveness, improved Income-Driven Repayment plans, and targeted assistance for hardship cases. This legislation represents a significant effort to make higher education more accessible and affordable, reducing financial stress and stimulating economic growth.

For federal student loan borrowers, understanding these changes and preparing proactively is essential. By knowing your loan types, reviewing your employment history, re-evaluating repayment plans, and staying informed through official channels, you can position yourself to take full advantage of these new opportunities. While challenges and criticisms exist, the expanded student loan forgiveness 2026 programs are a powerful step towards a future where educational debt no longer stands as an insurmountable barrier to success and well-being. This is a time of renewed hope for many, and with careful planning, it can translate into tangible financial freedom.