Student Loan Forgiveness 2026: Your Comprehensive Guide to Federal Programs

Student loan debt remains a significant burden for millions of Americans, impacting financial stability, career choices, and overall well-being. As we look towards 2026, understanding the landscape of federal student loan forgiveness programs and repayment options is more crucial than ever. This comprehensive guide aims to demystify these complex programs, providing clarity on eligibility, application processes, and strategic approaches to managing your student debt. Whether you’re a recent graduate, a seasoned professional, or someone contemplating higher education, gaining a firm grasp of these opportunities can significantly alleviate financial stress and pave the way for a more secure future.

Understanding the Evolving Landscape of Student Loan Forgiveness 2026

The policies surrounding student loans are dynamic, often subject to legislative changes, executive actions, and economic shifts. Staying informed about the latest developments is paramount. The year 2026 is on the horizon, and while specific details can evolve, the foundational federal programs for student loan forgiveness are expected to continue, albeit with potential modifications. Our focus here is to provide a robust framework of understanding, empowering you to navigate your options effectively.

The Core Federal Student Loan Forgiveness Programs

Several key federal programs offer pathways to student loan forgiveness. Each program is designed to assist specific groups of borrowers based on their profession, circumstances, or repayment history. Understanding the nuances of each is the first step toward determining your eligibility for student loan forgiveness 2026.

1. Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness (PSLF) program is arguably one of the most well-known and impactful forgiveness initiatives. It aims to encourage individuals to enter and remain in public service careers. Under PSLF, eligible federal student loans can be forgiven after 120 qualifying monthly payments (which do not have to be consecutive) while working full-time for a qualifying employer.

Who is Eligible for PSLF?

- Employment: You must be employed full-time by a U.S. federal, state, local, or tribal government organization, or a non-profit organization that is tax-exempt under Section 501(c)(3) of the Internal Revenue Code. Certain other non-profit organizations that provide specific public services may also qualify.

- Loan Type: Only Direct Loans are eligible for PSLF. If you have Federal Family Education Loan (FFEL) Program loans or Federal Perkins Loans, you would need to consolidate them into a Direct Consolidation Loan to become eligible.

- Repayment Plan: You must be repaying your loans under a qualifying income-driven repayment (IDR) plan. Standard repayment plans also qualify, but typically you would pay off your loan before reaching 120 payments.

- Payments: You must make 120 qualifying monthly payments. A qualifying payment is one made after October 1, 2007, under a qualifying repayment plan, for the full amount due as shown on your bill, no later than 15 days after your due date, and while you are employed full-time by a qualifying employer.

Applying for PSLF

The PSLF process involves several steps. It’s highly recommended to submit the PSLF Employment Certification Form annually or whenever you change employers. This form helps track your progress and ensures your employment and payments are being correctly counted. Once you’ve made 120 qualifying payments, you can submit the PSLF Application for Forgiveness.

For those interested in student loan forgiveness 2026 through PSLF, consistent tracking and communication with your loan servicer are key. Any changes in employment or loan status should be promptly updated.

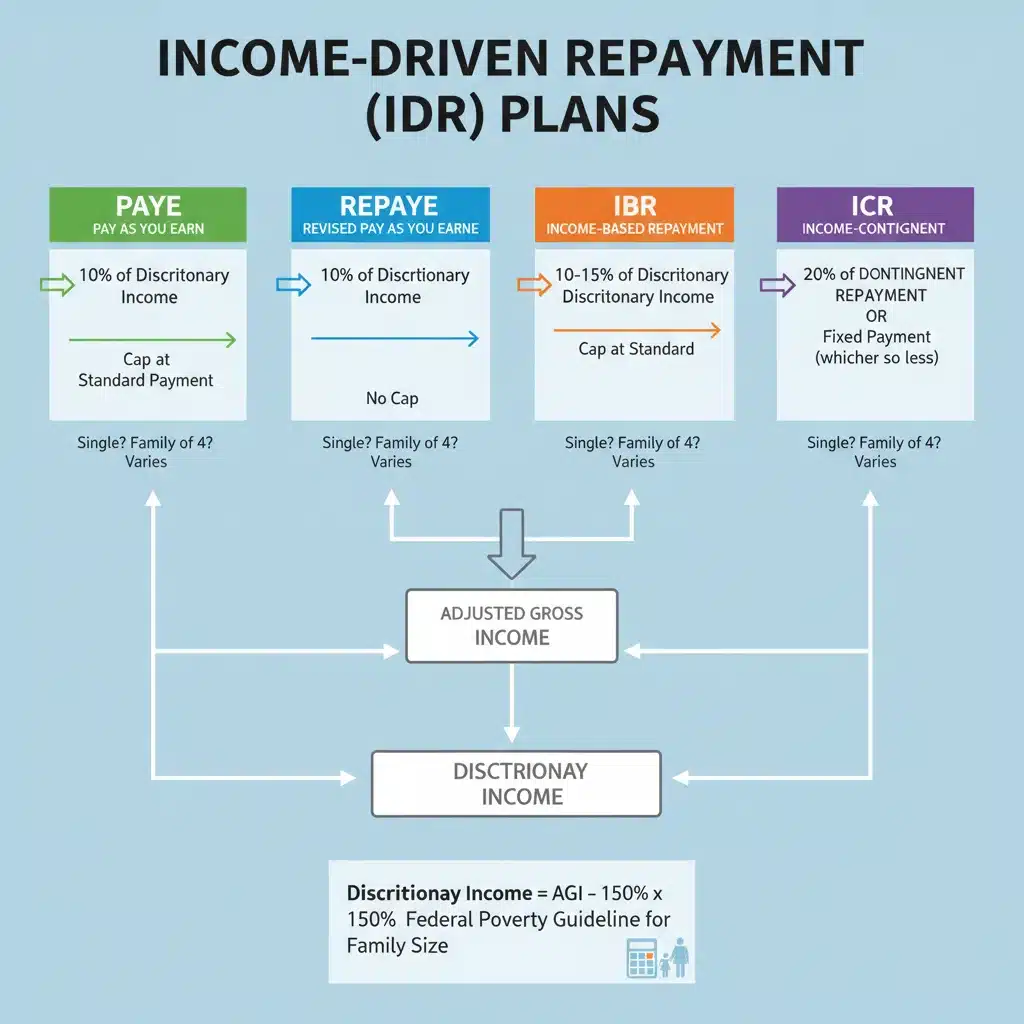

2. Income-Driven Repayment (IDR) Plan Forgiveness

Income-Driven Repayment (IDR) plans are designed to make student loan payments more manageable by capping them at a percentage of your discretionary income. A significant benefit of these plans is that any remaining loan balance is forgiven after 20 or 25 years of payments, depending on the specific plan and when you borrowed. While the forgiven amount may be taxable as income, these plans offer a long-term solution for borrowers struggling with high monthly payments.

Types of IDR Plans

- Revised Pay As You Earn (REPAYE) Plan: Generally 10% of discretionary income. Forgiveness after 20 years for undergraduate loans, 25 years for graduate loans.

- Pay As You Earn (PAYE) Plan: Generally 10% of discretionary income, but never more than the 10-year Standard Repayment Plan amount. Forgiveness after 20 years.

- Income-Based Repayment (IBR) Plan: Generally 10% or 15% of discretionary income, depending on when you received your first loans. Forgiveness after 20 or 25 years.

- Income-Contingent Repayment (ICR) Plan: The lesser of 20% of discretionary income or what you would pay on a repayment plan with a fixed payment over 12 years, adjusted according to your income. Forgiveness after 25 years.

- SAVE Plan (Saving on a Valuable Education): This new IDR plan, which fully replaced the REPAYE Plan, offers significantly lower monthly payments for many borrowers. Forgiveness timelines vary based on original loan balance, with some borrowers seeing forgiveness in as little as 10 years. This plan is particularly relevant for student loan forgiveness 2026 discussions.

It’s crucial to recertify your income and family size annually for IDR plans to ensure your payments are accurately calculated and to avoid capitalization of interest. The SAVE Plan is particularly noteworthy for its improved benefits, including preventing interest capitalization as long as you make your scheduled payments, and a more generous definition of discretionary income.

3. Teacher Loan Forgiveness

Teachers who work in low-income schools or educational service agencies may be eligible for forgiveness of up to $17,500 on their Direct Subsidized and Unsubsidized Loans and their Subsidized and Unsubsidized Federal Stafford Loans. To qualify, you must teach full-time for five complete and consecutive academic years in an eligible school or agency.

Eligibility for Teacher Loan Forgiveness

- School Eligibility: The school must be listed in the Teacher Cancellation Low Income (TCLI) Directory.

- Degree/Certification: You must be a highly qualified teacher.

- Loan Type: Direct Subsidized/Unsubsidized Loans, Subsidized/Unsubsidized Federal Stafford Loans.

The specific amount of forgiveness depends on the subject you teach. Highly qualified math and science teachers at the secondary level, and highly qualified special education teachers at the elementary or secondary level, can receive up to $17,500.

4. Perkins Loan Cancellation and Discharge

While the Federal Perkins Loan Program officially ended in 2017, existing Perkins Loans may still be eligible for cancellation or discharge under specific conditions based on your employment or other circumstances. These conditions include teaching in low-income schools, working as a special education teacher, certain public service roles (e.g., law enforcement, nurse, military service), or temporary/permanent disability.

5. Total and Permanent Disability (TPD) Discharge

Borrowers who are totally and permanently disabled may be eligible to have their federal student loans discharged. This discharge can be granted based on documentation from the U.S. Department of Veterans Affairs (VA), the Social Security Administration (SSA), or a physician.

TPD Discharge Eligibility

- VA Documentation: If the VA determines you have a service-connected disability that is 100% disabling.

- SSA Documentation: If you are receiving Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) benefits and your next scheduled disability review is within 5 to 7 years from your most recent SSA disability notice.

- Physician’s Certification: A physician certifies that you are unable to engage in any substantial gainful activity due to a physical or mental impairment that can be expected to result in death, has lasted for a continuous period of not less than 60 months, or can be expected to last for a continuous period of not less than 60 months.

It’s important to note that there is generally a three-year post-discharge monitoring period during which certain income and employment conditions must be met to finalize the discharge.

6. Borrower Defense to Repayment

This program allows for the discharge of federal student loans if a school engaged in misconduct, such as making misrepresentations about job placement rates, program quality, or accreditation. This relief is often applied to cohorts of students who attended specific institutions found to have engaged in widespread fraudulent practices. Keeping abreast of announcements from the Department of Education is vital if you believe you qualify under this provision, especially for student loan forgiveness 2026 related to past institutional issues.

7. Closed School Discharge

If your school closed while you were enrolled or shortly after you withdrew, you might be eligible for a closed school discharge, which forgives your federal student loans. To qualify, you generally must not have completed your program at another school or transferred your credits to another school.

Strategic Approaches to Federal Student Loan Repayment for 2026

Beyond forgiveness programs, several repayment strategies can significantly impact your financial health and accelerate your path to debt freedom. Understanding these options is key to making informed decisions about your student loan burden.

1. Consolidation of Federal Student Loans

Federal Direct Loan Consolidation allows you to combine multiple federal student loans into a single new loan with a single interest rate and one monthly payment. This can simplify your finances and, crucially, make otherwise ineligible loans (like FFEL or Perkins Loans) eligible for programs like PSLF or certain IDR plans. The interest rate of a Direct Consolidation Loan is the weighted average of the interest rates of the loans being consolidated, rounded up to the nearest one-eighth of one percent.

While consolidation can be beneficial, it’s essential to consider potential drawbacks, such as losing certain borrower benefits associated with your original loans or resetting the clock on IDR forgiveness if you consolidate loans that already have qualifying payments.

2. Understanding Interest and Capitalization

Interest capitalization is when unpaid interest is added to your loan’s principal balance. This increases the total amount you owe and means you’ll pay interest on a larger principal amount. Capitalization can occur in various situations, such as when you leave deferment or forbearance, or if you don’t recertify your income for an IDR plan on time. The SAVE Plan, as mentioned, offers a significant benefit by preventing interest capitalization as long as you make your scheduled payments, even if those payments don’t cover all the accrued interest.

3. Choosing the Right Repayment Plan

The standard repayment plan typically has a fixed monthly payment over 10 years. However, if this payment is unaffordable, exploring IDR plans is crucial. Use the Federal Student Aid Loan Simulator tool to compare different repayment plans and see how they affect your monthly payment, total interest paid, and potential forgiveness. This tool is invaluable for planning your student loan strategy for 2026 and beyond.

4. The Importance of Emergency Funds and Budgeting

While not a direct forgiveness program, having a robust emergency fund and a detailed budget are fundamental to managing student loan debt. An emergency fund can prevent you from needing to use forbearance or deferment, which can lead to interest capitalization and extend your repayment period. A budget helps you allocate funds effectively, potentially allowing you to make extra payments and reduce your principal faster.

Keeping Up with Policy Changes and Future Outlook for Student Loan Forgiveness 2026

The landscape of student loan relief is continually evolving. Government policies, economic conditions, and legislative priorities can all influence the availability and terms of forgiveness programs. It’s vital to remain informed through reliable sources:

- The official website of Federal Student Aid (studentaid.gov) is the definitive source for information on federal student loan programs.

- Regularly check announcements from the U.S. Department of Education.

- Stay informed about legislative proposals and actions that could impact student loan policies.

While we cannot predict exact policy changes for student loan forgiveness 2026, the general trend indicates a continued focus on making higher education more affordable and managing existing debt. This includes efforts to streamline existing programs and potentially introduce new relief measures.

Common Pitfalls to Avoid

- Ignoring Your Loans: Burying your head in the sand is the worst approach. Proactively managing your loans, even if it means contacting your servicer when you’re struggling, is crucial.

- Falling for Scams: Be wary of companies promising instant loan forgiveness for a fee. Official government programs do not require payment to apply for forgiveness. Always go through official channels.

- Not Recertifying IDR Plans: Failing to recertify your income and family size annually for IDR plans can lead to your payments increasing and unpaid interest capitalizing.

- Not Tracking PSLF Progress: For PSLF, consistent submission of the Employment Certification Form is essential to ensure your qualifying payments are being counted correctly. Don’t wait until you think you’ve made 120 payments to start checking.

- Defaulting on Loans: Defaulting on federal student loans has severe consequences, including wage garnishment, tax refund offset, and damage to your credit score. If you’re struggling, explore deferment, forbearance, or IDR plans before missing payments.

Key Considerations for 2026 and Beyond

As you plan for student loan forgiveness 2026, keep these considerations in mind:

- Tax Implications of Forgiveness: While most federal student loan forgiveness is currently tax-free through the end of 2025 due to the American Rescue Plan Act, this provision is set to expire. Unless extended, any forgiven amounts in 2026 and beyond (e.g., through IDR plans) may be considered taxable income by the IRS. It’s crucial to consult with a tax professional to understand your potential tax liability.

- Interest Rates: Federal student loan interest rates are set annually. While they don’t change for fixed-rate loans once disbursed, new loans or consolidated loans will reflect the prevailing rates. Keep an eye on these rates as they can impact your total repayment cost.

- Economic Conditions: Broader economic trends can influence government policy and the job market, which in turn can affect your ability to repay loans or qualify for certain programs. Staying abreast of economic forecasts can help you make proactive financial decisions.

A Step-by-Step Guide to Navigating Your Options for Student Loan Forgiveness 2026

- Identify Your Loan Types: Determine if you have federal or private student loans. Federal loans offer a wider range of forgiveness and repayment options. You can find this information on studentaid.gov.

- Understand Your Current Repayment Plan: Know your current monthly payment, interest rate, and remaining balance. Access this information through your loan servicer’s website.

- Assess Your Eligibility for Forgiveness Programs: Review the criteria for PSLF, Teacher Loan Forgiveness, IDR forgiveness, and other specific programs. Consider your profession, employer, and repayment history.

- Explore Income-Driven Repayment (IDR) Plans: If your payments are unaffordable, use the Loan Simulator on studentaid.gov to compare IDR plans, particularly the new SAVE Plan. This can significantly reduce your monthly burden and put you on a path to forgiveness.

- Consider Consolidation: If you have older federal loans (FFEL, Perkins) or multiple federal loans, consolidation might be beneficial to qualify for more programs or simplify payments. Be aware of potential drawbacks.

- Stay Organized and Keep Records: Maintain thorough records of all loan documents, communication with your servicer, and proof of employment (especially for PSLF). This is critical for any application or dispute.

- Recertify Annually: If you are on an IDR plan, remember to recertify your income and family size every year to keep your payments accurate and prevent interest capitalization.

- Seek Professional Advice: For complex situations, consider consulting a non-profit credit counselor specializing in student debt or a financial advisor. Be cautious of for-profit companies charging fees for services you can get for free from the Department of Education.

- Stay Informed: Regularly check studentaid.gov for updates on policies, program changes, and new relief initiatives, especially as we approach and enter 2026.

Conclusion: Empowering Your Journey to Student Debt Relief

Navigating the world of student loan forgiveness and repayment options can feel overwhelming, but it doesn’t have to be. By understanding the core federal programs, strategically choosing your repayment path, and staying informed about policy changes, you can take control of your student debt. The goal is not just to manage payments but to find a sustainable path toward financial freedom, with student loan forgiveness 2026 being a significant milestone for many.

Remember, proactive engagement with your loan servicer and the Department of Education is your best asset. Don’t hesitate to ask questions, explore all available resources, and advocate for your financial well-being. The journey to debt relief is a marathon, not a sprint, and with the right knowledge and strategy, you can successfully navigate it.