Maximize Social Security 2026: Boost Payouts 15% with Key Strategies

Understanding and optimizing your Social Security benefits is one of the most critical aspects of retirement planning. For those eyeing retirement in the coming years, or even those already receiving benefits, the landscape of Social Security is ever-evolving. As we look towards 2026, there are specific updates, strategies, and considerations that can significantly impact your monthly payouts. This comprehensive guide aims to equip you with the knowledge to maximize Social Security 2026 benefits, potentially increasing your payments by 15% or more through informed decisions and strategic planning.

Social Security is more than just a government program; it’s a foundational pillar of financial security for millions of Americans. However, its complexities often lead to missed opportunities for maximizing benefits. From understanding your Full Retirement Age (FRA) to navigating spousal benefits and the impact of continued earnings, every decision counts. The goal here isn’t just to receive your Social Security; it’s to ensure you’re receiving every dollar you’re entitled to, and then some.

The Evolving Landscape of Social Security: What to Expect in 2026

The Social Security Administration (SSA) regularly adjusts its rules and benefit calculations to account for economic changes, inflation, and demographic shifts. While specific details for 2026 are still being finalized, historical trends and current projections offer valuable insights. Key areas to watch include the Cost-of-Living Adjustment (COLA), changes to the earnings limit, and potential shifts in the Full Retirement Age for future retirees.

Cost-of-Living Adjustment (COLA)

The COLA is a crucial factor in determining how much your benefits will increase each year. Designed to help Social Security benefits keep pace with inflation, the COLA is announced annually in October and takes effect in January of the following year. While the 2026 COLA won’t be known until late 2025, it’s a vital component of benefit growth. A robust COLA can contribute directly to a higher monthly payout, helping you maximize Social Security 2026. Staying informed about economic forecasts and inflation rates can give you an educated guess about the potential COLA, allowing for better personal financial projections.

Changes to the Earnings Limit

For those who claim Social Security benefits before their Full Retirement Age and continue to work, an earnings limit applies. If your earnings exceed this limit, a portion of your benefits will be temporarily withheld. This limit typically increases each year. Understanding the 2026 earnings limit is critical for anyone planning to work while receiving benefits, as it directly impacts your net Social Security income. Once you reach your Full Retirement Age, the earnings limit no longer applies, and you can earn as much as you want without affecting your benefits.

Full Retirement Age (FRA) Considerations

Your Full Retirement Age (FRA) is the age at which you are entitled to receive 100% of your primary insurance amount (PIA). This age varies depending on your birth year. For individuals born in 1960 or later, the FRA is 67. Claiming benefits before your FRA results in a permanent reduction, while delaying beyond your FRA (up to age 70) results in an increase. There are no current proposals to change the FRA for those approaching retirement in 2026, but it’s a concept fundamental to maximizing your benefits.

Core Strategies to Maximize Social Security 2026 Benefits

Achieving a 15% increase in your Social Security payouts isn’t a pipe dream; it’s a realistic goal with strategic planning. Here are the core strategies to help you maximize Social Security 2026:

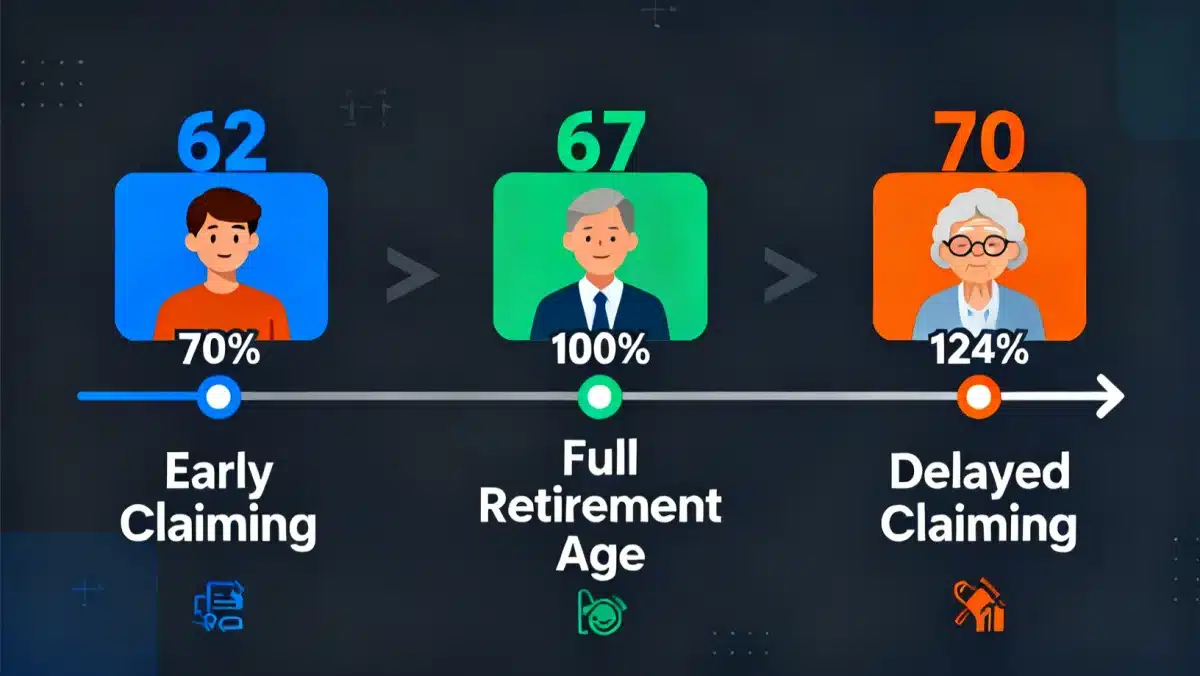

1. Optimize Your Claiming Age

This is arguably the most impactful decision you’ll make regarding your Social Security benefits. While you can start collecting benefits as early as age 62, doing so comes with a significant reduction – up to 30% permanently. Conversely, delaying beyond your FRA, up to age 70, can increase your benefits by 8% per year. This delayed retirement credit is a powerful tool for boosting your monthly income.

The Power of Delaying Claims

Consider this: if your FRA is 67 and your primary insurance amount (PIA) is $2,000, claiming at 62 would reduce your benefit to approximately $1,400. Delaying until 70, however, would increase your benefit to $2,640 (132% of your PIA). That’s a difference of $1,240 per month! Over a 20-year retirement, this adds up to hundreds of thousands of dollars.

The decision of when to claim is highly personal and depends on several factors:

- Health and Longevity: If you expect to live a long life, delaying benefits often pays off significantly.

- Current Financial Needs: Do you need the income immediately, or can other savings cover your expenses?

- Spousal Considerations: Your claiming age can impact your spouse’s benefits.

- Other Income Sources: Do you have pensions, 401(k)s, or other investments to rely on?

For many, delaying just a few years past their FRA can provide a substantial boost. Even delaying from 62 to 65 can make a noticeable difference. Use the SSA’s online tools and consider consulting a financial advisor to run personalized scenarios.

2. Understand and Leverage Spousal Benefits

If you are married, divorced, or widowed, spousal benefits can significantly enhance your household’s total Social Security income. These benefits allow eligible individuals to claim a percentage of their spouse’s (or ex-spouse’s) Social Security record, even if they have little or no work history of their own.

Spousal Benefits for Married Couples

A spouse can claim up to 50% of their partner’s primary insurance amount (PIA) if they claim at their own Full Retirement Age. If they claim earlier, this amount is reduced. It’s crucial to note that your spouse must generally have already filed for their benefits for you to claim spousal benefits. However, there are exceptions and specific rules, especially if your spouse is delaying their claim.

Divorced Spousal Benefits

You may be able to claim benefits on an ex-spouse’s record if:

- Your marriage lasted 10 years or longer.

- You are currently unmarried.

- You are age 62 or older.

- Your ex-spouse is entitled to Social Security retirement or disability benefits.

- The benefit you would receive based on your own work record is less than the benefit you would receive on your ex-spouse’s record.

Crucially, your ex-spouse does not need to have filed for their benefits for you to claim, provided you’ve been divorced for at least two years. This can be a powerful strategy to maximize Social Security 2026 without impacting your ex-spouse’s benefits.

Survivor Benefits for Widows and Widowers

If your spouse passes away, you may be eligible for survivor benefits, which can be up to 100% of the deceased spouse’s benefit amount if you claim at your FRA. You can start survivor benefits as early as age 60 (or age 50 if you are disabled). A common strategy is for the surviving spouse to claim survivor benefits early while letting their own earned benefit grow until age 70, then switching to their higher personal benefit. This strategy is known as “file and suspend” for survivor benefits, and it’s a key way to maximize Social Security 2026 for widows and widowers.

3. Understand the Impact of Your Work History

Your Social Security benefit is based on your highest 35 years of earnings. To maximize Social Security 2026, it’s essential to understand how your work history contributes to this calculation.

Filling in the 35 Years

If you have fewer than 35 years of earnings, zero-earning years will be averaged into your calculation, significantly lowering your benefit. If you’re approaching retirement and have gaps in your work history, consider working a few extra years to replace those zero-earning years with higher-earning ones. Even if you’ve already worked 35 years, continuing to work in a high-earning year can replace a lower-earning year from earlier in your career, thereby increasing your average and your monthly benefit.

Review Your Earnings Record

It’s vital to regularly check your Social Security earnings record for accuracy. Errors can occur, and missing or incorrect earnings can lead to lower benefits. You can access your earnings statement online through your My Social Security account. If you find discrepancies, contact the SSA immediately to rectify them.

4. Coordinate Benefits with Your Spouse

For married couples, coordinating when each spouse claims benefits can lead to a higher combined lifetime payout. This often involves one spouse claiming earlier while the other delays, or one spouse claiming spousal benefits while their own benefit grows.

Strategic Claiming for Couples

- Higher Earner Delays: Generally, the higher-earning spouse should delay claiming benefits as long as possible, ideally until age 70. This maximizes the larger benefit, which will also form the basis for survivor benefits for the lower-earning spouse.

- Lower Earner Claims Early or Spousal: The lower-earning spouse might claim their own benefits earlier, or claim spousal benefits if it’s more advantageous, providing some income while the higher earner’s benefit grows.

- “File and Suspend” (Limited Application): While the original “file and suspend” strategy for individuals was largely eliminated, a form of it remains for survivor benefits. For married couples, the strategy of one spouse claiming spousal benefits while their own record grows to 70 is still viable under specific conditions.

These strategies are complex and require careful analysis of individual circumstances, including age differences, health statuses, and expected longevity. A financial advisor specializing in Social Security can be invaluable here.

Advanced Considerations and Potential Pitfalls

Beyond the core strategies, there are several advanced considerations and potential pitfalls to be aware of when you maximize Social Security 2026.

Taxation of Social Security Benefits

Depending on your combined income, a portion of your Social Security benefits may be subject to federal income tax. “Combined income” is defined as your adjusted gross income (AGI) plus non-taxable interest plus one-half of your Social Security benefits. If your combined income exceeds certain thresholds ($25,000 for single filers, $32,000 for married filing jointly), up to 50% or even 85% of your benefits could be taxable. Planning your retirement withdrawals from other accounts (e.g., Roth vs. traditional IRAs) can help manage your combined income and potentially reduce your Social Security taxation.

Medicare Premiums and Social Security

If you’re enrolled in Medicare, your Part B and Part D premiums are typically deducted directly from your Social Security benefits. For higher-income beneficiaries, an Income-Related Monthly Adjustment Amount (IRMAA) can significantly increase these premiums. This means that while you’re working to maximize Social Security 2026, you also need to consider how your income impacts your Medicare costs, as these deductions can reduce your net benefit.

The “Do-Over” Option: Withdrawing Your Application

If you claimed benefits within the last 12 months and regret your decision, you have a one-time opportunity to withdraw your application. You would need to repay all benefits received, including any benefits paid to family members on your record. This allows you to reapply at a later date, potentially at a higher age, to receive a larger monthly benefit. This can be a lifesaver if your financial situation changes unexpectedly after you’ve started receiving benefits.

Suspending Benefits

If you’ve reached your Full Retirement Age and are receiving benefits, you can choose to suspend them. This allows your benefits to accrue delayed retirement credits, increasing your monthly payment when you decide to restart them (up to age 70). This can be a good option if you return to work or find you no longer need the income temporarily, and want to boost your future payments. You cannot suspend benefits if you are receiving spousal or survivor benefits, or if you are under your FRA.

Tools and Resources to Aid Your Planning

The Social Security Administration provides a wealth of online tools and resources that are invaluable for planning how to maximize Social Security 2026.

My Social Security Account

Creating a My Social Security account is a must. This online portal allows you to:

- View your earnings record.

- Get estimates of your future benefits at different claiming ages.

- Review your benefit statement.

- Apply for benefits online.

- Manage your current benefits if you’re already receiving them.

Regularly checking your earnings record is crucial to ensure accuracy and prevent any potential discrepancies that could affect your future benefits.

Benefit Calculators

The SSA offers various benefit calculators (e.g., Retirement Estimator, Life Expectancy Calculator) that can help you model different claiming scenarios and understand the long-term impact of your decisions. Independent financial planning websites also offer sophisticated calculators that can factor in more variables, such as taxation and other retirement income sources.

Professional Financial Advice

Given the complexity and personalized nature of Social Security planning, consulting a qualified financial advisor with expertise in retirement and Social Security strategies is highly recommended. They can help you:

- Analyze your specific situation and goals.

- Run detailed scenarios for different claiming ages and strategies.

- Coordinate Social Security with your other retirement assets.

- Navigate the application process and avoid common mistakes.

- Provide guidance on tax-efficient withdrawal strategies.

The investment in professional advice can often pay for itself many times over in increased lifetime Social Security benefits.

Common Mistakes to Avoid When Claiming Social Security

Even with the best intentions, many people make mistakes that leave money on the table. Avoiding these common pitfalls is key to successfully maximizing your benefits.

Claiming Too Early Without a Plan

The most frequent mistake is claiming benefits at age 62 simply because it’s the earliest option, without fully understanding the permanent reduction this entails. While early claiming is right for some (e.g., those with severe health issues or immediate financial distress), it should be a deliberate decision, not an default one.

Not Understanding Spousal and Survivor Benefits

Many couples fail to coordinate their claiming strategies, or individuals miss out on valuable spousal or survivor benefits they are entitled to. These benefits can significantly boost household income, yet they are often overlooked or misunderstood.

Ignoring Your Earnings Record

Failing to review your Social Security earnings record can lead to lost benefits if there are errors or omissions. Your benefit is based on your earnings, so ensuring their accuracy is paramount.

Not Re-evaluating Decisions

Life circumstances change. What seemed like the right claiming strategy at 62 might not be ideal at 65. Not taking advantage of the “do-over” option (if eligible) or suspending benefits when circumstances allow, means missing opportunities to increase your payments.

Failing to Factor in Taxation and Medicare

Focusing solely on the gross Social Security benefit without considering the impact of federal income tax and Medicare premiums (especially IRMAA) can lead to an inflated expectation of your net retirement income. Holistic planning is essential.

Conclusion: Your Path to Maximizing Social Security 2026

The journey to maximize Social Security 2026 benefits is a strategic one, requiring careful planning, ongoing vigilance, and a thorough understanding of the rules. By optimizing your claiming age, leveraging spousal and survivor benefits, ensuring your work history is accurate, and coordinating your strategy with your spouse, you can significantly enhance your retirement income.

Aiming for a 15% increase in your Social Security payouts is an ambitious but achievable goal for many. It might involve delaying your claim by a few years, strategically utilizing spousal rules, or ensuring you’ve maximized your earning years. The key is to start planning early, utilize the resources available from the SSA, and consider seeking professional guidance to tailor a strategy that fits your unique financial situation and retirement aspirations.

Don’t leave money on the table. Take proactive steps now to understand the intricacies of Social Security and make informed decisions that will secure a more prosperous and comfortable retirement for you and your loved ones. The benefits of a well-executed Social Security strategy will be felt for decades to come.

Limits Guide")